Book #5/52: The Intelligent Investor - Benjamin Graham

I'm not that intelligent after all

Statistics

Date Read: 25 Jan - 13 Feb

Pages: 640

Format Read: NLB Paperback

Genres: Non-Fiction, Finance

My Rating(out of 5): 4 stars

Review

If I had a dollar for every time The Intelligent Investor has been recommended when someone asks “What should I read to learn more about Investing?”, I probably wouldn’t need to care so much about learning how to invest.

This book is as close as it comes to a cult classic on its subject. Even if you’ve never heard of its author, Benjamin Graham, you almost definitely know of his most famous student — Warren Buffett — who regards the book as “by far the best book on investing ever written”.

What, then, makes it so special? It’s not that it provides a foolproof get-rich-quick scheme through investments. Rather, it is because Graham’s writing stood the test of time remarkably well since first published decades ago in 1949, in a field where what has worked and what works now hardly continues to work years or even months later.

In this book, “the father of value investing” aims to “supply, in a form suitable for laymen, guidance in the adoption and execution of an investment policy”. Much is thus centred around his policy of Value Investing — to only buy a stock at a price deemed undervalued relative to the business’s earnings, assets, and other business factors. He outlines some strategies and indicators which different types of investors can use to achieve this.

Apart from that, he gives his opinion on various kinds of financial instruments, and analyses how different economic factors would affect results. All these arguments are backed by countless historical examples. Two whole chapters are even dedicated to comparing and analysing multiple past case studies.

Quite frankly, the best thing reading this book did was that it humbled me. To give you some context, I’ve been fooling around with investing since the middle of 2021, putting a portion of my monthly NS allowance into different parts of the stock market. I thought that this experience (and the googling that came with it) would make me at least a novice investor.

It turns out that in Graham’s eyes, I wouldn’t be much more than a speculator. Sure, I wasn’t borrowing money to invest or day trading like the most extreme examples cited. Still, neither was I doing my due diligence in researching companies like a business owner would. I was also guilty of many of the practices he looked upon with disdain — buying into airline stocks because I believed air travel was going to rise, for instance. Thus, I realised how much I truly don’t know. This helped me be more realistic as to my stock-picking ability, and stop my overconfident, under-analysed investment decisions.

Of course, I only realised that there was so much I didn’t know because the book opened my eyes to things I never knew existed or understood the meaning of. The more you learn, the less you know. Thus, the obvious benefit I gained was knowledge of new financial terminology (P/E ratio, book value, etc.), applicable strategies (Dollar-cost averaging, rebalancing), and historical trends (past bull and bear markets).

Moreover, I found the wealth of analysis on real-world data quite instructive. The case studies on markets in the early 1970s and 2000s provided the necessary evidence to show that what Graham wrote in 1949 still held true. They also let me visualise how Graham’s strategies were used. I even could try to analyse the data myself.

Overall, this book really changed my mindset towards investment. I regret not reading it earlier because that could’ve prevented some of my mistakes.

However, I felt that it was quite lengthy and repetitive at times. In this aspect, the footnotes and commentary by Jason Zweig at the end of every chapter helped greatly to summarise and explain things in a more recent (though still 20 years ago) context. Thus, if you’re someone just starting out, I recommend you get the most recent version with the commentary. It also helps with determining which parts are outdated and not so relevant to the average investor. Honestly, I think that without the newer commentary, I would’ve knocked my rating down half a star.

Ultimately, this might not be the best first read to learn about investment. I was struggling quite a bit with the combination of the new terminology and older writing (though that could just be me), which explains the 3 weeks I took to read it.

After powering through though, I could feel that it did impact my thinking quite a bit and gave me many new insights. Thus, I think that it’s still a worthwhile read. Just be warned it may not be the easiest one, especially if you’re a beginner like me.

Favourite Quotes

To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks.

If you merely try to bring just a little extra knowledge and cleverness to bear upon your investment program, instead of realizing a little better than normal results, you may well find that you have done worse.

However, we must point out a troublesome paradox here, which is that the mathematical valuations have become most prevalent precisely in those areas where one might consider them least reliable.

The speculative public is incorrigible. In financial terms it cannot count beyond 3. It will buy anything, at any price, if there seems to be some “action” in progress. It will fall for any company identified with “franchising”, computers, electronics, science, technology, or what have you, when the particular fashion is raging.

Yesterday’s losers are often tomorrow’s winners

Notes + Key Takeaways

“Buy low, sell high” seems like incredibly simple advice, but most people inadvertently do the opposite.

When we see a stock’s price rising, we think that it’ll continue to do so, and vice versa. Thus, it’s human nature to buy when prices are high and sell when they are low — the exact opposite of what’s sensible. Thus, the intelligent investor must suppress human instinct and other natural feelings of fear and FOMO, to buy in a bear market and sell in a bull market instead.

Most “investors” are mere “speculators”

The concept of Investors vs Speculators appears often in this book. Graham argues that an investor has to meet these three criteria:

Thorough analysis of a company and the soundness of its underlying business before purchasing its stock

Deliberately protecting yourself against serious losses

Aspiring for “adequate”, not extraordinary, performance

Thus, anyone who day trades, invests on margin, or buys based on hype or superior current and future performance (or any other superficial, feel-based factors) is not investing, but speculating.

Most experts/investment funds don’t beat the market in the long run

In fact, less than 15% have beaten the market over 20 years up till 2002. If even those who do it for a living often fail, it is incredibly difficult for an individual investor to consistently do so.

Don’t think of diversification as reducing your gains. Rather, think of it as increasing the chances of you making gains.

If it was possible to always pick the right stocks, diversification would only reduce gains compared to a portfolio of all the winners. But of course, it’s not possible to always pick the “next Microsoft”. Thus, diversification instead helps to reduce the chances of missing out on the next big winner, thus increasing the chances of profiting.

Prospects for future growth may not translate into increases in stock prices

We often think that industries of the future, such as artificial intelligence and biotechnology, have the greatest potential for growth in their stock price. However, these future growth prospects are often already priced in. Stocks in these industries are often even overpriced because almost everyone buys into their prospects for future growth.

It is easy to match the market, but requires much more effort just to beat it by a little consistently

Index funds and Exchange Traded Funds are an example of the ease of matching the market’s returns. These funds hold a basket of stocks in a given industry based on the market share, thus by buying into them, you will match the returns of that industry.

For instance, the S&P 500 ETF holds all the stocks in the Standard & Poor 500 Index proportional to their size. Thus, just owning that fund ensures that you will match the index’s returns (less the ~0.1% expense ratio). Whereas figuring out which companies in the index will perform the best takes a lot more effort, and your predictions may not be right.

It is impossible to invest based on prediction. Investing based on protection is the better choice.

This is the core idea behind Graham’s value investing. What does he mean by this?

Often, we invest in what we think will generate the most returns in the future. However, doing that accurately is an impossible task. Thus, it is more sensible to invest to minimise the chances of undue losses in the future, by ensuring you don’t overpay for an overvalued stock.

Don’t neglect inflation

Inflation will eat into the real value of investment returns. When inflation rises, bonds become less attractive because their absolute yields stay the same, and thus their real yields drop. Stocks are only half a hedge against this, because there isn’t much correlation between high inflation and high stock prices. Other instruments such as Real Estate Investment Trusts (REITs) and Treasury Inflation-Protected Securities (TIPS) are options to protect against inflation.

“Loss aversion” has its merits

One common concept in psychology and behavioural economics is that of loss aversion — people avoid losses because it feels more painful than a gain of an equivalent percentage. However, this holds some merit in the world of investment. If a stock drops by a certain percentage, it would require a bigger gain to reach its original share price. If it drops by 50%, it needs a 100% gain. If it drops by 75%, it requires a 300% gain. And humans are more likely to think in percentage, or relative, terms than in absolute terms.

Portfolio allocation should not be merely based on age

A common rule of thumb is to allocate (100-age)% of your portfolio into stocks, and the rest into bonds. Proponents of this suggest that since stocks are more volatile but rise more in the long run, younger people are able to benefit from owning more of them.

However, this ignores their risk appetite, and the potential need for withdrawing investments in the near future. If someone were to suddenly need emergency funds 5 years on after investing in a portfolio full of stocks, he may find that he no longer has the amount he needs because the stock market is down. On the flip side, the wealthy elderly can still benefit from investing in stocks — or rather, their children can — because they may not need the money.

There are no “good” or “bad” stocks, only cheap or expensive stocks

Even if a company is in superb health, its stock would not be a good buy if the price is too high.

Growth stocks are “glamour” type investments

Many index funds tout themselves as “growth funds”. However, these growth stocks run largely on hype. Many of them lack the earnings and past track records to back up their high prices. Their popularity also makes them far more volatile. Thus, looking for value instead of chasing growth is always the safer and more sensible option.

Don’t neglect dividends

Many companies now don't give dividends, arguing that their profits would be better used if they were put back into the company to invest in increasing future earnings. Shareholders have gradually accepted this “daddy knows best” policy too. However, research has shown that companies which hold onto earnings instead of distributing part of them as dividends tend to do more poorly, implying that the profits are, in fact, not better utilised. Thus, Graham recommends looking at stocks of companies that distribute around 2/3 of their earnings via dividends, and have a good record (20 years uninterrupted) of dividends.

Analysis should be based on concrete arithmetic figures, not future predictions and gut feel

Nowadays, greater emphasis is placed on future earnings. All sorts of complicated formulas are used to provide the most precise estimate of future earnings and thus stock prices. However, as mentioned in Quote #3 above, the problem with this is that these formulas are used to calculate something that’s inherently unpredictable. All the complicated mathematics does is trick us into thinking that these estimates of the future are reliable.

Instead, Graham recommends that security analysis be based on a few fundamental indicators and simple calculations. Some of them are:

P/E ratio: Ratio of the price of a company’s stock to its earnings per share. Graham recommends that P/E should be <15

Book value: asset values - liabilities. A key characteristic of a value stock is that its book value per share is less than its share price. This way, you are paying essentially nothing for the company’s growth prospects, and paying at a discount to the company’s worth for ownership.

Earnings to fixed charges: whether earnings can cover bond payments (usually good to be >5 times pretax)

Earnings growth: Increase in at least 1/3 (33%) per share earnings in the past 10 years. 3-year averages should be used rather than earnings of a single year.

Price to asset ratio: Ratio of share price to company’s asset value. Recommended to be <1.5x

Financial statements and indicators may not be accurate

There are many instances of companies “cooking their books”, cunningly obscuring their reports with difficult language or special allowances. For instance, they might report repeated costs as one-off spending, thus artificially increasing their earnings. Thus, it is paramount for investors to always take reported figures with a pinch of salt, and look through footnotes and back pages when doing an analysis of business statements.

Thus, when doing calculations to attain the indicators I’ve listed above, it’s also important to scrutinise the values provided.

The market is mostly efficient

Graham uses the famous “Mr. Market” analogy to illustrate this.

The Intelligent Investor controls their emotions

Succeeding in investing is less about being a genius, and more about being disciplined to stick to principles and strategies even in the highest bull market and the lowest bear market. In fact, intelligent investors are excited when prices crash and worried when they skyrocket.

Pay less attention to the prices of your holdings

Especially for defensive (passive) investors who don’t wish to analyse financial statements like a second job. Some people (me included) have the bad habit of choosing the passive strategy, and then proceeding to check the prices of their funds multiple times a day. This compulsive extra step doesn’t help much, and may even do more harm than good by causing you to be swayed and sell or buy unnecessarily.

Selecting your own stocks is not necessary (or even advisable) for the average “defensive investor”

Other (far less stressful) strategies

Dollar-cost averaging: Putting a set amount every month into an index fund/ETF. This way, you buy more shares when the market is low and less when prices are high, reducing your risk of choosing the wrong time to invest.

Set allocation investing: Setting a specific allocation (e.g. 50-50 stocks to bonds), and rebalancing when the ratios change. When one component rises, it will take up a bigger ratio — thus you sell it to bring the ratio back down. When it falls, buy more of it to bring the ratio up. This way, you will automatically be buying stocks when prices are low and selling when they are high.

If you’re in a similar position (young or with limited income and knowledge), you might find my thoughts below relevant! Else, feel free to skip it.

My personal takeaways:

As someone who doesn’t have pretty little capital and knowledge of the stock market, I’ve come to the realisation that the effort I’ll have to put into picking my own investments just wouldn't be worth the return currently.

Why is that so?

Firstly, I will have to put far more hours into learning how to analyse business fundamentals due to my lower starting point of knowledge. Secondly, with my limited capital, the return I would get would be quite insignificant.

For instance, a 3% increase in returns from my additional knowledge on a $10k portfolio would only net $300. I would most probably be better off spending some of that time and effort on educating myself and improving my soft skills. After all, education is the best investment. Focusing on that would most likely have a bigger impact on my finances when I’m young and lack capital, because that would increase my initial employability.

Thus, I’ve decided to only keep the stocks that meet most of the book’s criteria. I will then focus on the two (more passive) strategies, ETFs, and Index funds instead. Of course, this doesn’t mean that I’ll completely stop learning about this topic. I’ll continue reading up (on stock analysis and how to decide what to pick), but just not put it into action as much until I’ve accumulated more knowledge and capital. One strategy I might follow is to make ETFs the bulk of my portfolio (say, 90%), and only choose stocks (“speculate”) with the remaining funds.

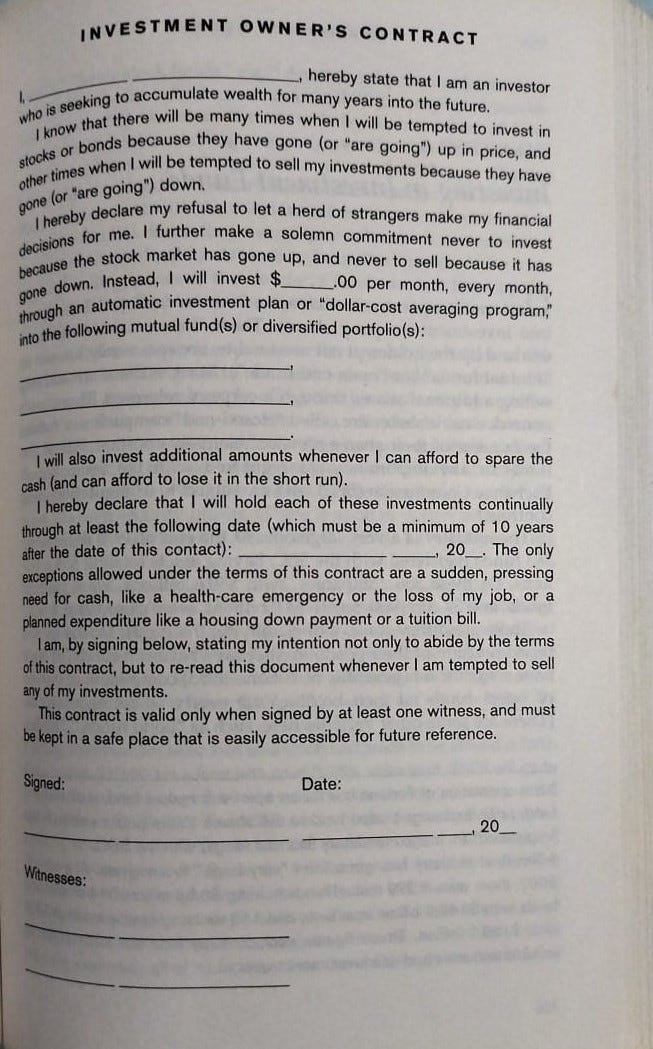

I shall also follow this investment owner’s contract: